Page Resources: About this Page | How to Navigate | The Impact of COVID-19 | Share Feedback

The ABC Data Exchange

Healthcare

and Wellness

The uninsured are often one serious illness or accident away from financial crisis.

Health insurance acts as a protective factor against unexpected healthcare costs that can damage an individual’s or a family’s ability to maintain assets.

Health insurance is provided in two major forms, employer-based health insurance, predominant for adults, and Medicaid and Medicare for those age 65 and over.

The measures on this page highlight levels of employer-provided health insurance and uninsurance rates among residents in Forsyth County.

Literature Review Highlights

Even when controlling for income and education, wealth is associated with better self-rated health. [1]

Assets are associated with a reduction in family stress generally. [2]

High debt is associated with mental disorders, and the relationship between debt and mental disorder is much stronger than the relationship between income and mental disorder. However, the study does not attempt to disentangle which way causation runs: does debt cause mental disorder, do those with mental disorders rack up more debt, or is it a little of both? [3]

Literature Review References

[1] Pollack, C. E., Cubbin, C., Sania, A., Hayward, M., Vallone, D., Flaherty, B., & Braveman, P. A. (2013). Do wealth disparities contribute to health disparities within racial/ethnic groups?. J Epidemiol Community Health, 67(5), 439-445.

[2] Rothwell, D. W., & Han, C. K. (2010). Exploring the relationship between assets and family stress among low‐income families. Family Relations, 59(4), 396-407.

[3] Jenkins, R., Bhugra, D., Bebbington, P., Brugha, T., Farrell, M., Coid, J., … & Meltzer, H. (2008). Debt, income and mental disorder in the general population. Psychological medicine, 38(10), 1485-1493.

Major Findings

Employer-based health insurance rates were lower for Black and Hispanic/Latino residents and residents with lower levels of educational attainment.

Uninsurance rates have decreased significantly since 2011 in Forsyth County, but uninsurance rates remain especially high for residents who have a high school diploma or less and residents who identify as Hispanic/Latino.

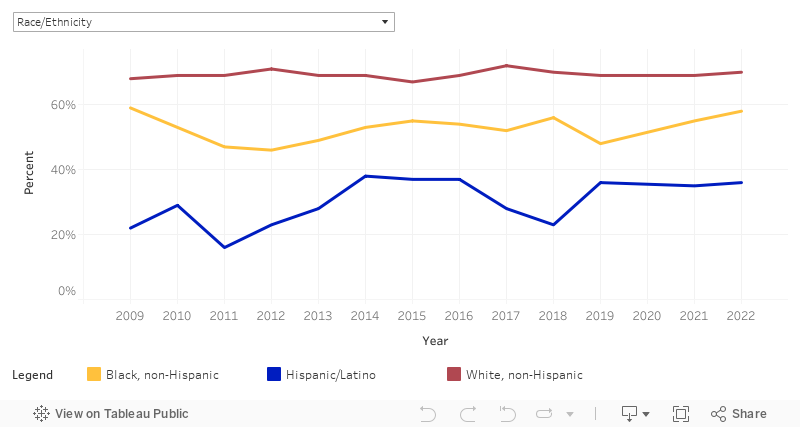

Employer-Provided Health Insurance

Although the Affordable Care Act (ACA) expanded access to health insurance for individuals without employer-provided coverage, most American working adults still receive health insurance through their employers [1]. Employer-sponsored plans often have lower upfront costs than individual market plans and may offer broader coverage, though subsidies can make Marketplace plans more affordable for some enrollees [2,3]. View data notes for this measure.

Data Visualization

Employer-Provided Health Insurance (Forsyth County, 2023)

Use the dropdown menu below to view data on different groups.

Key Takeaways

Overall, from 2009 to 2023, the rate of employer-provided health insurance for working adults (ages 18-64) remained stable.

Forsyth County’s rates have ranged between 58% and 64% since 2009.

Major disparities in employer-provided health insurance by race/ethnicity have persisted.

In 2023, 72% of White adults had employer-provided coverage, compared to 61% of Black adults and 43% of Hispanic/Latino adults.

Adults with higher educational attainment were more likely to have employer-provided health insurance.

In 2023, 79%-88% of adults with a Bachelor’s Degree or higher had employer-provided coverage, compared to 41% of those with a high school diploma or less.

Residents with lower household incomes were less likely to have employer-provided health insurance.

Nearly 80% of adults with household incomes greater than $100,000 had insurance through their employer in 2023, compared to 19% with household incomes of $20,000 or less.

Data Notes

Employer-Provided Health Insurance

- Although there is a disparity in employer-provided health insurance rates by race/ethnicity, the margin of error for Hispanic/Latino residents is high, so exact percentage differences should be interpreted with caution across all years.

- Similarly, income groups at $60,000 or less have high margins of error in most years, while estimates for those with an Associate’s Degree have higher margins of error, specifically in 2022 and 2023, requiring the same caution.

References

- U.S. Census Bureau. (2024). Health Insurance Coverage in the United States: 2023. Retrieved from https://www.census.gov/library/publications/2024/demo/p60-284.html

- Kaiser Family Foundation. (2023). 2023 Employer Health Benefits Survey. Retrieved from https://www.kff.org/report-section/ehbs-2023-summary-of-findings/

- U.S. Government Accountability Office [GAO]. (2023). Private Health Plans: Comparison of Employer-Sponsored Plans to Healthcare.gov Marketplace Plans. Retrieved from https://www.gao.gov/products/gao-25-106798

Data Source

- U.S. Census Bureau. (2024). American Community Survey (ACS), 1-Year Public Use Microdata Sample (PUMS), 2009-2019 and 2021-2023. Retrieved from Public Use Microdata Sample (PUMS).

Uninsured Individuals

Health insurance provides important protection for a household’s assets by reducing expenses incurred from a medical emergency or the treatment of a chronic illness that might otherwise require a family to spend down long-term savings, sell off assets, or go into debt. In addition, because health insurance coverage encourages people to seek preventive care and treatment for injuries and illnesses, it minimizes the impact a major injury or illness would otherwise have on an individual’s ability to earn income. The uninsured are often one serious illness or accident away from a financial crisis.

While the Affordable Care Act (ACA) significantly reduced the uninsured rate, millions of Americans still lack coverage, including low-income individuals who fall into the coverage gap as a result of some states’ decisions not to expand Medicaid under ACA. Further, repealing the ACA’s individual mandate has made it so there is no longer a financial penalty for not having health insurance coverage [1]. View data notes for this measure.

Data Visualization

Uninsured Individuals (Forsyth County, 2023)

Use the dropdown menu below to view data on different groups.

Key Takeaways

Overall, uninsured rates have decreased significantly over time.

Across all comparison communities, fewer people lacked insurance in 2023 than in 2009. In Forsyth County, the uninsurance rate peaked at 18% in 2011 but declined to 11% in 2023.

Working-age residents had the highest uninsurance rate in 2023.

The uninsurance rate was 16% for adults 18-34 and 14% for those 35-64, while 7% of children under 18 and 2% or less of adults 65 and older were uninsured.

Major disparities were present by race/ethnicity.

In 2023, nearly one-third (31%) of Hispanic/Latino residents were uninsured, compared to 10% of Black residents and 5% of White residents.

Residents with lower educational attainment had the highest uninsurance rates.

In 2023, 24% of residents with a high school diploma or less were uninsured, compared to 12% of those with some college, 9% with an Associate’s Degree, and 3% with a Bachelor’s Degree or higher.

More males (15%) than females (9%) were uninsured in 2023.

Data Notes

Uninsured Individuals

- On December 1, 2023, North Carolina expanded its Medicaid program to cover more residents ages 19 to 6. Due to the timing of this expansion, the data in this measure does not yet reflect its impact.

- Although there is a disparity in uninsurance rates by race/ethnicity, the margin of error for Hispanic/Latino residents is high in 2010, 2011, and 2013, so exact percentage differences should be interpreted with caution.

References

- Prosperity Now.

Data Source

- U.S. Census Bureau. (2024). American Community Survey (ACS), 1-Year Public Use Microdata Sample (PUMS), 2009-2019 and 2021-2023. Retrieved from Public Use Microdata Sample (PUMS).

About the ABC Data Exchange

Welcome to the ABC Data Exchange (ABCDE), part of the Asset Building Coalition's website. This resource is made up of six interconnected web pages which, together, offer in-depth data and context on the issue of Asset Poverty in Forsyth County, North Carolina.

The landing page of the ABCDE introduces the issue of Asset Poverty, and the impact it has on individuals and families in our community. Five additional, topic-specific data deep dive pages offer a broader range of data and contextual information.

The Asset Building Coalition's purpose and goals in producing this web-based resource are to:

- Build a hub of local information on financial wellbeing and asset poverty to be used as a tool for community stakeholders.

- Educate and raise awareness locally about asset poverty, its upstream causes, and the effects it has on individuals and our community overall.

- Highlight key issues, challenges, and disparities among core measures of asset poverty to catalyze local conversations about innovative and equitable solutions.

The Asset Building Coalition has produced this content in partnership with Forsyth Futures, a registered 501(c)(3) organization that provides action-oriented data analysis and reporting services to organizations within Forsyth County. If you have questions about this content, please contact info@abcforsyth.org.

Some measures in the ABC Data Exchange are based on modeled estimates

Some measures contained in the Data Exchange use estimates that are not solely based on local data. These estimates use local demographic and other information to predict local estimates based on analyst modeling of state-level data. That is, estimates are calculated at a state level that is then adjusted to local demographics.

Specific measures that are based on modeled estimates are clearly labeled within the data exchange.

The Impact of COVID-19

In 2020 and 2021, the COVID-19 pandemic dramatically reshaped how our community functions and it disrupted many aspects of our day-to-day lives. Many people experienced impacts to health and safety, increased stress, and many lost some or all of their ability to earn income. These and many other impacts on our community have tested our resolve, impacted our well being, and almost certainly changed the circumstances around our financial wellbeing in ways we don’t yet understand.

All of the data contained in this web-based informational resource is pre-pandemic; for more specific information, view the data notes that are available for each measure. These measures will be updated with 2020 data in late 2021, once that data becomes available.

If you have questions about the data contained in this informational resource, please contact info@forsythfutures.org.